Highlights

- The Mega Backdoor Roth allows business owners to contribute after-tax money to their 401(k) and convert it into a Roth IRA.

- This strategy helps high earners leverage higher contribution limits for more retirement savings.

- Roth accounts offer tax-free growth, which is beneficial if you expect a higher tax bracket later.

- Not all 401(k) plans allow after-tax contributions or in-service conversions, which may complicate the process.

As a business owner, saving for retirement is crucial. One powerful strategy you might want to explore is the Mega Backdoor Roth as a business owner. It allows you to contribute significantly more to a Roth account, which grows tax-free, helping you maximize your retirement savings. But how exactly does this strategy work, and is it fit for your retirement planning?

In this blog post, we’ll discuss how the Mega Backdoor Roth works and whether it’s a viable strategy for business owners looking to save more for retirement.

What is a Mega Backdoor Roth?

The Mega Backdoor Roth as a business owner lets you contribute after-tax money to your 401(k) and convert it into a Roth IRA or 401(k). With standard contribution limits, high earners can sometimes feel restricted. Still, this strategy helps you leverage the higher total contribution limit, which includes employee contributions, employer contributions, and after-tax contributions.

How Does the Mega Backdoor Roth Work?

To use the Mega Backdoor Roth as a business owner, here are the key steps:

- Make After-Tax Contributions: You start by making after-tax contributions beyond your usual pre-tax or Roth 401(k) contributions.

- Convert to a Roth Account: After making those contributions, you convert them into a Roth 401(k) or IRA for tax-free growth.

- Tax-Free Growth: Once inside a Roth account, your money grows tax-free, offering long-term benefits, especially if you expect to be in a higher tax later.

Why Should Business Owners Consider a Mega Backdoor Roth?

If you’re a business owner, you likely have more control over your retirement plan than the average employee, especially if you have a solo 401(k) or a custom retirement plan for your business. Here are some key reasons you might want to consider the Mega Backdoor Roth IRA:

- Higher Contribution Limits: One of the biggest advantages of the Mega Backdoor Roth is that it allows you to contribute much more than a traditional Roth IRA, which is limited to $6,500 per year ($7,500 if you’re over 50). As a business owner, you may have more disposable income for retirees. This strategy lets you do that in a tax-advantaged way.

- Tax-Free Growth: Instead of paying taxes on your withdrawals in retirement, you can enjoy tax-free income.

- Flexibility: If you own a business, you have more flexibility when setting up your retirement plan. This could mean more options for making after-tax contributions or converting them into a Roth account.

Are There Any Downsides to the Mega Backdoor Roth?

While the Mega Backdoor Roth has a lot of advantages, it’s not without its challenges. Here are a few things to consider before deciding if this strategy is right for you:

- Plan Restrictions: Not all 401(k) plans allow after-tax contributions or in-service conversions (which let you move the money into a Roth while still working). You’ll need to check with your plan administrator to see if these options are available.

- Complexity: The Mega Backdoor Roth can be complicated to execute, especially if you’re unfamiliar with retirement savings. You may need to work with a financial advisor or tax professional to ensure you follow all the rules and properly take advantage of the strategy.

- Tax Implications: While the goal is to convert your after-tax contributions to a Roth account without paying additional taxes, any earnings on those contributions could be taxable when you make the conversion. You’ll need to keep a close eye on the timing of your conversion to minimize taxes.

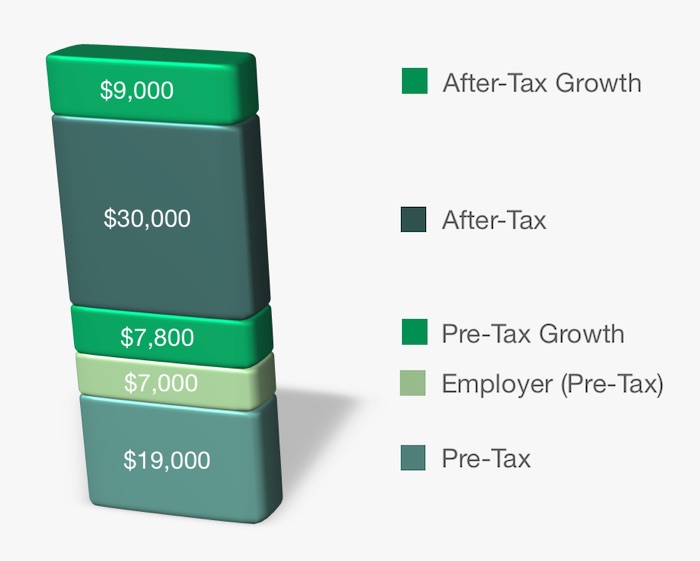

How Much Can You Contribute Through a Mega Backdoor Roth?

As of 2024, the mega backdoor Roth lets you save up to $69,000 ($76,500 if you’re 50 or older) in your 401(k) for 2024.

Here’s how it works: The standard 401(k) contribution limit is $23,000 ($30,500 for those 50 and older). On top of that, you can add up to $46,000 in after-tax contributions, but if your employer offers a match, you’ll need to subtract their contribution from that $46,000 limit.

Is the Mega Backdoor Roth Right for You?

Opting for Mega Backdoor Roth as a business owner could be the perfect tool to maximize your retirement savings. But it’s not the right fit for everyone. Here are a few questions to ask yourself before deciding if this strategy is right for you:

- Do you have enough disposable income to make after-tax contributions? If you’re already maxing out your 401(k) contributions and have extra income to spare, the Mega Backdoor Roth could be a great way to save more.

- Does your 401(k) plan allow after-tax contributions and in-service conversions? If your plan doesn’t allow these options, you may need to explore other retirement strategies.

- Are you comfortable with the complexity of this strategy? The Mega Backdoor Roth can be tricky, so you must be comfortable handling the rules and potential tax implications.

Summary

Considering Mega Backdoor Roth as business owner could be the best way to supercharge your retirement savings. It allows you to contribute more to your Roth accounts, giving you the benefit of tax-free growth and withdrawals in retirement. If you’re unsure, consulting with a financial advisor can help determine if this strategy aligns with your retirement goals.

At Blackstone Commodity, we focus on building strategic relationships between our industry expertise and the specialized knowledge of our partners. Our clients benefit from self-directed IRA investment options in precious metals through STRATA Trust, which holds over $3B in assets, and Equity Trust Company, which oversees $34B, including gold IRA investing and cryptocurrency investments.

Disclaimer

The content provided on this blog is for informational and educational purposes only and does not constitute financial or investment advice. While we strive to provide accurate and up-to-date information, you should not rely on this content as a substitute for professional financial advice. Any financial decisions you make are done so at your own risk, and we encourage you to consult with a licensed financial advisor before making any investment decisions.

The views and opinions expressed in this blog are solely those of the authors and do not necessarily reflect the views of any affiliated entities. The information presented here is not intended as a solicitation or recommendation to buy, sell, or hold any financial product.